Key Takeaways

- Electricity demand is soaring due to AI, electric vehicles, and the push to modernize aging infrastructure, turning forward-looking utility companies into innovation-driven growth stories.

- Nuclear power’s resurgence has been led by bipartisan support, advances in reactor technology, and streamlined regulatory changes that facilitate licensing.

- Even in the face of policy shifts, breakthrough innovations in solar energy are making it cheaper, smarter, and more scalable, opening doors to long-term investment potential.

- The Syntax Power Solutions Index provides exposure to clean energy-focused utilities and leaders in solar, nuclear, hydrogen, and smart grid technologies — sectors driving the future of power generation and infrastructure.

Overview

After decades of relatively flat electricity demand in the U.S., utilities are increasingly investing in technology and renewable energy to address rising electricity needs, with global demand expected to triple by 2050.1 This surge is driven by the rapid growth of electric vehicles, AI-powered data centers, industrial reshoring and manufacturing, and the expanding digitization of energy — including widespread use of sensors and advanced technologies to upgrade, manage, and optimize the grid. Utilities, once seen as low-risk, low-growth, and dividend-focused stocks, are becoming innovation platforms as they reduce the reliance on fossil fuels in favor of more climate friendly alternatives.

To better measure this growing opportunity, we constructed the Syntax Power Solutions Index. The index provides exposure to US-listed clean energy companies involved in nuclear, solar, wind power and natural gas (a relatively cleaner fossil fuel) power generation, and those that manufacture the equipment that support these power sources. It also encompasses companies advancing hydrogen and fuel cell ecosystems, biofuels, and smart grid technologies.

This paper highlights the characteristics of the next-generation energy space as seen through the Syntax Power Solutions Index. To start, we examine three key components that will drive the energy industry over the next several decades: the expansion of the electrical grid, the reemergence of nuclear energy, and the role of solar energy.

Expanding The Grid

Future energy solutions depend on more affordable, cleaner renewable sources, along with a modernized electric grid capable of efficiently delivering and storing power where it's needed most. The current grid has many challenges, as much of it was built in the 1960s without renewable energy in mind. Renewable energy often needs to be transmitted over long distances as it is often generated far away from where people live. Wind and solar energy sources are also intermittent, creating the need for more advanced energy storage solutions to make it available on demand.2

Breakthrough Energy, a network of entities founded by Bill Gates to accelerate the world's transition to a clean energy future, has stated electric grid capacity must triple by 2050 to meet expected demand. In May, the Federal Energy Regulatory Commission approved landmark regulations that support this required growth. Key components of the regulations include:

- Requiring grid operators to plan transmission infrastructure for 20 years into the future.

- Providing guidelines on cost sharing for utility lines that cross state lines to reduce potential bottlenecks.

- Streamlining planning and permitting rules to support implementation.

- Placing enhanced emphasis on grid stability to better withstand extreme weather.3

Nuclear Energy Gains Momentum

Nuclear energy was historically associated with regulatory complexities, cost overruns, construction delays and public opposition – and, as a result, poor investment returns. Now, nuclear energy is experiencing a powerful resurgence as governments and utilities are turning to nuclear power as a reliable, low-carbon backbone for future energy systems. In the US, Congress passed the ADVANCE Act, which will modernize the Nuclear Regulatory Commission (NRC) and streamline the process for licensing new Generation 4 nuclear reactors, though considerable challenges remain for the industry to hit its targets.4

The growth in nuclear power is not limited to the US: more than 20 nations, including the U.S., pledged to triple installed nuclear power by 2050 during last year’s COP28 climate conference.5

Nuclear energy has been making frequent headlines, with notable news stories such as:

- The Department of Energy is backing the restart of shuttered nuclear plants like Palisades in Michigan.6

- Microsoft has signed a 20-year agreement to purchase power from a planned restart of the Three Mile Island Unit 1 reactor which was decommissioned in 2019.7

- According to the IAEA, around 100 nuclear reactors worldwide have already received life extension licenses following safety upgrades and refurbishments.8

Technical innovations and public-private partnerships are also contributing to the expansion of nuclear energy and are likely to continue. Examples include:

- The TerraPower nuclear plant under construction in Wyoming is a blueprint for clean and efficient nuclear plants. It is backed by a $2 billion public-private partnership with the U.S. Department of Energy through the Advanced Reactor Demonstration Program (ARDP), and features state-of-the-art reactor and energy storage technologies, along with a modular design.9

- Small modular reactors provide a compact and scalable approach to energy production as they can be manufactured in a factory setting and transported to the site where they are needed.

- Ongoing nuclear power research, which is advancing on many fronts — including fuel cell innovation, nuclear battery development, and the use of AI in reactor management to enhance safety, streamline maintenance, and optimize performance.10

Although fusion reactors remain years from commercialization, they are the focus of active research and development. Unlike today’s fission reactors, which generate energy by splitting atoms, fusion produces energy by combining atoms with the benefit of not creating long-lived radioactive waste. Often called the 'holy grail' of energy, fusion promises clean, safe, and virtually limitless power, though such capabilities have been on the horizon for the better part of 70 years.

Solar Energy: Policy Headwinds and Technological Tailwinds

The One Big Beautiful Bill Act, signed into law in July 2025, aims to boost domestic fossil fuel production. At the same time, the bill significantly rolls back clean energy incentives that were in the Inflation Reduction Act. In the solar energy sector, tax credits are being phased out on an accelerated schedule. The 30% residential investment tax credit is set to expire at the end of 2025, while eligibility for commercial solar projects will decline to 60% in 2027, drop to 20% in 2028, and be eliminated entirely by 2029. The looming expiration of tax credits has triggered a rush to “safe harbor” projects by locking in incentives before the 2026 deadline.11

On the positive side, solar costs have dropped by 80% since 2010 for utilities.12 In many regions, solar is now the cheapest source of new electricity generation — even without incentives — reaching what's known as 'grid parity’. Technical innovation serves as a potential offset to policy headwinds as it continues to drive efficiencies and lower costs while increasing the applications of where and how solar energy can be used.

For example:

- Perovskite Tandem Cells are lightweight, flexible, and offer potential efficiency gains of 30% or higher, which is a material increase from present solar panel efficiency levels of about 22%. Pilot production of this technology is underway, with mass production planned for 2026-2027 and broad market availability targeted for 2027-2028. 13

- Other technology innovations on the horizon include AI-powered smart solar systems that enhance efficiency and grid responsiveness, transparent solar panels which can be integrated into windows and building facades, and integrated solar and battery storage systems.

The Power Solutions Opportunity

We use the Syntax Power Solutions Index to quantify the opportunity set for the future energy space. The index selects from companies listed on the NYSE and Nasdaq exchanges, including ADRs. Each holding must meet size and liquidity standards (including a minimum market cap of $50 million, a 20% free float, and $1 million average daily trading volume in the trailing 90 days) and must have more than 50% of their revenue tied to one of the eligible thematic groups: Clean Energy, Hydrogen and Fuel Cells, Biofuels, or Smart Grid. The index is equally weighted, reconstitutes and rebalances quarterly, and presently holds 89 securities.

The index construction process leverages Syntax’s FIS® industry classification system to identify company exposures down to product-line revenue. This provides enhanced precision when targeting companies with the desired traits. Moreover, FIS® also allows the Index to be studied from multiple perspectives beyond traditional sectors.

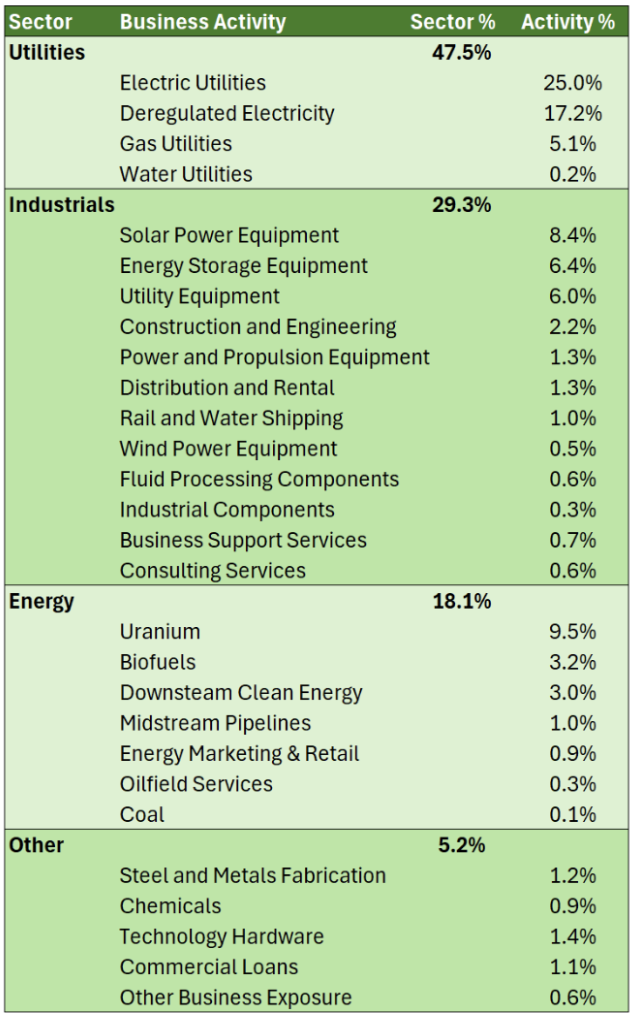

Exhibit 1 highlights that 95% of the Index’s exposure is to three sectors: Utilities (48%), Industrials (29%), and Energy (18%). Within Utilities, slightly more than half the exposure is to Electric Utilities (25% of the Index) which are regulated entities that often are monopolies in certain geographic regions. These utilities need approval from regulators for rate changes, and they are allowed to earn a return on their capital that is set by state regulators. In contrast, Deregulated Electric Utilities (17% of the index) set prices based on market conditions and therefore focus on efficiency, innovation, and often M&A activity that supports their growth.

The 29% allocation to Industrials includes exposure to a variety of infrastructure-related business activities, such as Solar Power Equipment (8.4%), Energy Storage Equipment (6.4%), and Utility Equipment (6.0%), along with smaller allocations to other equipment, consulting, and construction-related business lines.

Exhibit 1: Syntax Power Solution Index Sector and Business Activity Exposure

The Energy sector allocation (18%) is slightly more than half concentrated in Uranium-related holdings, represented by nine companies in the Index that engage in the mining and refining of this metal used in nuclear power generation. Roughly 3% is allocated to both Biofuels and Downstream Clean Energy, the latter of which focuses on Renewable Natural Gas Synthesis and Hydrogen.

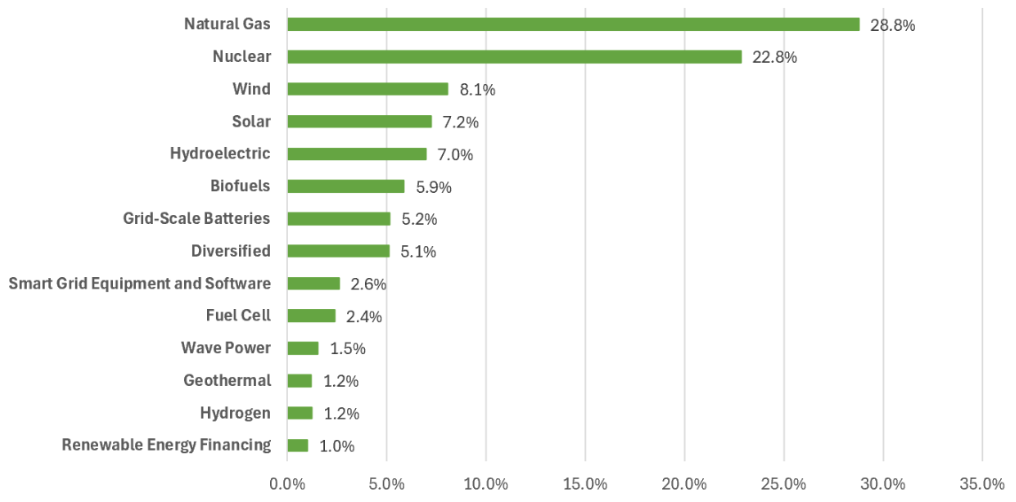

The graph in Exhibit 2 uses Syntax’s granular classification data to map each company’s exposure to specific energy sources or technologies.

Exhibit 2: Syntax Power Solutions Index Holdings By Energy Source and Technology

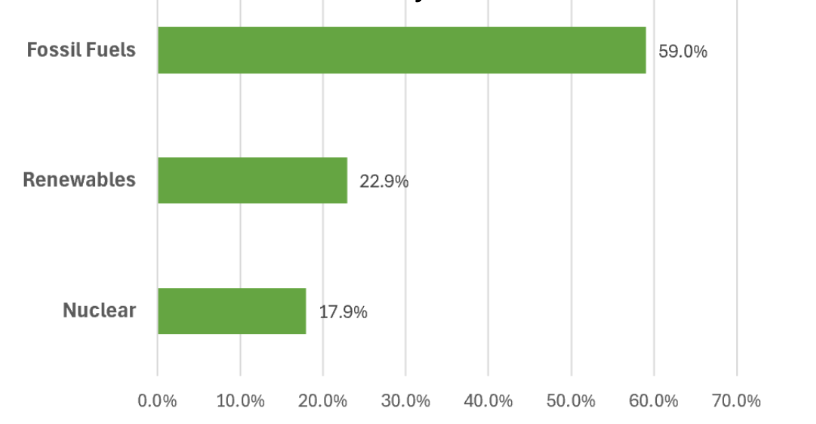

The graph shows that 71% of the Index’s revenue is associated with renewable energy and businesses related to the grid, with the remaining 29% balance tied to natural gas. The focus on renewables aligns well with where the energy industry is headed. Recent data shows in the first third of 2025, which precedes the passage of the One Big Beautiful Bill Act which this article acknowledges as a threat to the adoption rate of renewables, 96% of all new utility-scale electricity generating capacity added in the U.S. has been allocated to renewables — with 78% going to solar and 18% to wind.14 This is meaningfully different from the present state of U.S. electricity generation by source as shown in Exhibit 3. The graph underscores that fossil fuel, at 59% of U.S. electricity generation, is still the majority energy source.

Exhibit 3: Exhibit 3: US Electric Generation By Source

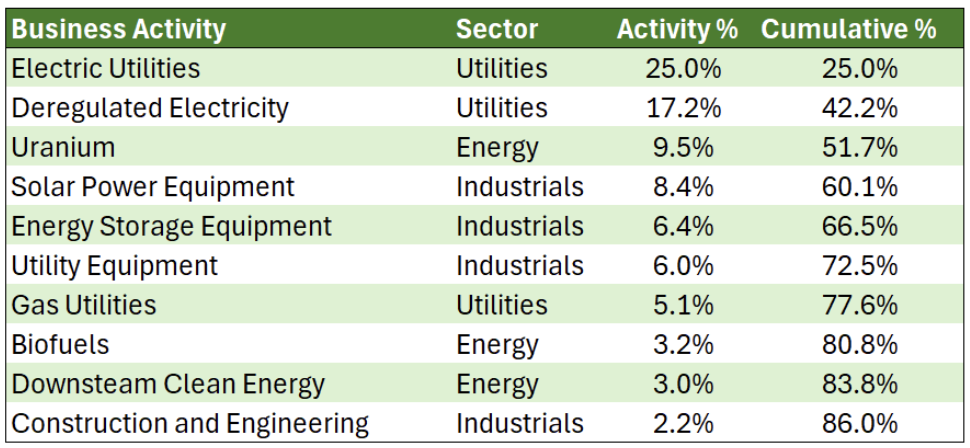

Overall, the Index has allocations to 28 distinct business lines. Exhibit 4 shows that the top 10 activities account for 86% of the Index’s revenue.

Exhibit 4: Top 10 Business Activities of the Syntax Power Solutions Index

Utilities are the hub of the US energy infrastructure, so it is not surprising that the two largest business activities in the Index are Electric Utilities and Deregulated Electricity. It is worth reiterating:

- The Utilities in the Index have at least 50% of their revenue tied to clean energy, making them industry leaders in this regard.

- The Syntax Power Solutions Index has roughly 40% of its total Electric Utility exposure in Deregulated Utilities (17% weight relative to 42% for all Electric Utilities). As a reference point, the S&P 500 has a 2.2% weight to Electric Utilities, of which about 25% (or less than 1% of the total) is in Deregulated Utilities.

Allocations to Uranium (10%), Solar Power Equipment (8%), and Energy Storage Equipment (6%) round out the top 5 business activities, which in total represent two thirds of the Index. The remaining 23 business activities provide diversifying exposures across one third of the Index.

Conclusion

There is little business that can be conducted without a source of energy, and the growth of future energy needs is undeniable. In spite of this, energy remains underrepresented in most portfolios – it represents just 3% of the S&P 500 while it is close to 6% of GDP.15 The move to renewable energy is well underway, supported by two observation points:

- Renewables experienced a 30% growth rate in 2024.16

- Renewables represent 96% of new energy capacity added in 2025.17

The Syntax Power Solutions Index takes a forward-looking approach to understanding this compelling part of the economy, designed to capture companies driving the future of power generation and infrastructure. Wayne Gretzky, one of the greatest hockey players of all time, once said:

"I skate to where the puck is going to be, not where it has been."

This quote encapsulates the core philosophy behind the Syntax Power Solutions Index: it is designed not to mirror the legacy energy sector, but to anticipate and position for the future of power generation and infrastructure. To learn more, please reach out to sgrieco@syntaxdata.com or visit our website https://www.syntaxdata.com/.

- Breakthrough Energy: The State of the Transition 2023

- FERC shakes up power industry with landmark grid rule - E&E News by POLITICO

- L389 The State of the Transition.pdf

- canarymedia.com/articles/nuclear/20-plus-countries-pledge-to-triple-the-worlds-nuclear-energy-by-2050

- HOLTEC PALISADES | Department of Energy

- Inside Microsoft & Constellation's Power Purchase Agreement | Procurement Magazine

- Nuclear Plant Life Extensions Help Clean Energy Transition| IAEA

- Understanding TerraPower’s Natrium Reactor Design and Demonstration Project Progress

- https://www.msn10-breakthroughs-in-nuclear-energy-that-could-change-the-future

- Analysis based on reporting from Forbes (May 2025) and EnergySage, reflecting industry responses to recent changes under the One Big Beautiful Bill Act

- How much has the cost of renewable energy fallen by since 2010? | World Economic Forum

- Hanwha Q Cells eyes tandem cell mass production in 2027 - KED Global

- FERC: Solar + wind made up 96% of new US power generating capacity in first third of 2025 | Electrek

- https://ycharts.com/indicators/us_energy_expenditures_as_share_of_gdp

- Deloitte Power and Utilities Industry Outlook

- FERC: Solar + wind made up 96% of new US power generating capacity in first third of 2025 | Electrek