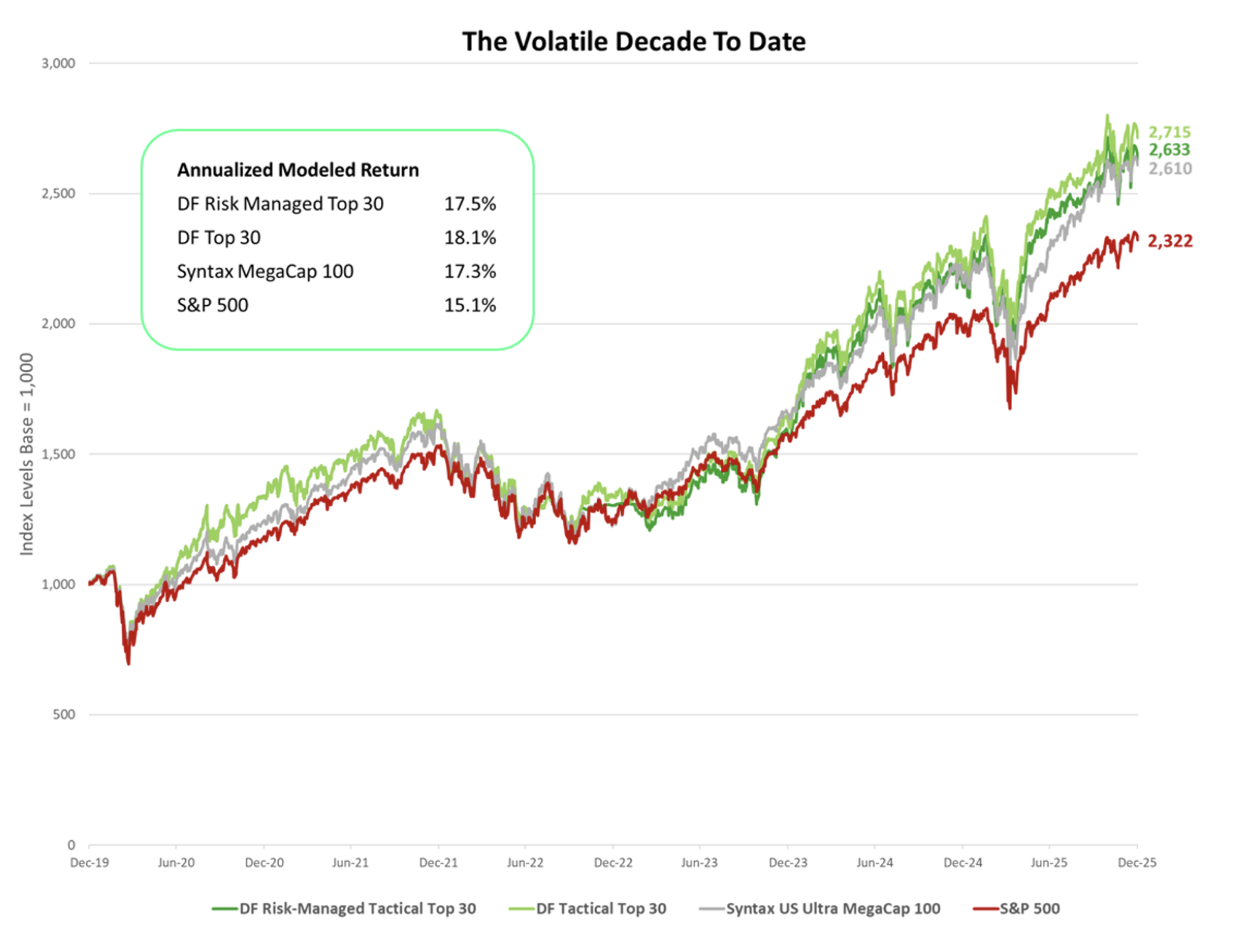

A practical look at two-state allocation and regime signals in risk-managed equity

Managing equity risk through exposure adjustments raises an important design question: how should those adjustments be implemented? If exposure is intended to change as market conditions evolve, the structure of the allocation framework becomes a central element of the strategy.

Some approaches scale exposure incrementally, gradually reducing or increasing equity allocations as conditions change. Others rely on discrete allocation states that shift more decisively between risk-on and risk-off environments. The DF Risk-Managed Tactical Top 30 Index (DF RMT30) follows the latter approach, using a two-state allocation framework that moves fully between equities and short-term U.S. Treasuries.

This structure reflects a deliberate design choice. Rather than continuously adjusting exposure, the framework responds only to sustained changes in market conditions, distinguishing clearly between environments where equity exposure is appropriate and those where risk reduction is warranted.

Binary allocation and regime identification

The allocation framework underlying DF RMT30 operates through two distinct states. At any point in time, the index is fully allocated either to its equity portfolio or to short-term U.S. Treasuries. Allocation changes occur only when predefined signals indicate a sustained shift in the broader market trend.

Exhibit 1 illustrates this conceptual structure. The framework identifies transitions between risk-on and risk-off environments using observable market signals rather than discretionary decisions. When trend conditions deteriorate sufficiently, the index shifts from equities to Treasuries. When conditions improve, the allocation returns to equities.

Exhibit 1: Conceptual binary allocation framework

This design serves two purposes. First, it avoids the complexity and potential instability associated with frequent incremental allocation changes. Second, it helps ensure that the strategy remains clearly aligned with prevailing market regimes rather than reacting to short-term price fluctuations.

In practice, this means allocation changes occur relatively infrequently and are typically associated with extended periods of market stress rather than routine volatility.

Why exit and re-entry signals are asymmetric

An important feature of the framework is that the signals governing exit from equities and re-entry into equities are intentionally asymmetric. Different signal thresholds are used depending on whether the index is currently allocated to equities or to Treasuries.

This asymmetry reflects the different risks associated with exiting equity markets versus re-entering them. Exiting too early during temporary market volatility may cause a strategy to miss subsequent recoveries, while re-entering too quickly during a downturn may expose the portfolio to further declines.

To address these competing risks, the allocation framework monitors longer-term trend conditions when equities are held, identifying sustained market deterioration before shifting to Treasuries. When the index is allocated to Treasuries, intermediate-term signals are used to identify meaningful improvements in market conditions before re-entering equities.

This design aims to avoid reacting to short-term market noise while still allowing the allocation to respond to persistent changes in market direction.

Allocation behavior across market environments

The practical implications of this design become clearer when viewed across historical market environments. Because the framework engages only during sustained changes in market trend, the index spends the majority of time allocated to equities.

Exhibit 2 summarizes the historical distribution of allocation states, showing the proportion of time the index has historically remained invested in equities versus short-term Treasuries.

Exhibit 2: Historical time spent in equities and short-term U.S. Treasuries

This pattern reflects the intended role of the allocation framework. The objective is not to trade frequently or to respond to short-term volatility, but to alter exposure during extended periods of market deterioration.

Exhibit 3 provides additional context by illustrating how these allocation shifts have affected drawdown and recovery dynamics across major market cycles.

Exhibit 3: Allocation Framework Impacts by Market Cycle

During prolonged equity downturns, changes in exposure can meaningfully alter both the depth of drawdowns and the speed of recovery once market conditions stabilize. During sustained bull markets, the index remains fully allocated to equities, allowing the underlying equity portfolio to drive performance.

A design choice centered on regime behavior

The binary allocation structure and asymmetric signal design reflect a broader philosophy about how equity risk should be managed. Rather than attempting to continuously fine-tune exposure in response to short-term market movements, the framework focuses on identifying sustained shifts in market regimes.

This approach emphasizes clarity and discipline in allocation decisions. Equity exposure remains fully engaged during most favorable market environments, while meaningful reductions occur only when broader market conditions deteriorate.

Viewed in this context, the allocation framework serves as the mechanism through which exposure-based risk management operates. By responding to persistent changes in market trend rather than short-term volatility, the strategy seeks to balance participation in equity advances with protection during extended downturns across market cycles.

The next article shifts from strategy design to portfolio application, examining how exposure-managed equity strategies may fit within long-horizon institutional portfolios.